By David Stockman

The starting point for understanding the delusional fantasy of the present moment is this: The mainstream narrative is so corrupted by greed, sloth, group think and will to power that it has become a risible caricature of itself. In plain english, what is held to be true by the powers-that-be is flat-out unreliable, unhinged and unsustainable.

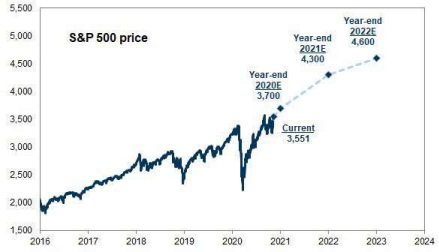

For instance, bubble vision is jawing giddily this morning about the new stock market forecast from Goldman’s chief equity strategist, David Kostin. According to this overpaid genius, the silver bullet of a Covid vaccine is now assured owing to the Pfizer announcement (but see the debunking below), so we will soon be back to normal and the stock market will soar to 4,300 on the S&P by the end of next year (2021).

So back up the trucks!

That’s a 25% gain (with dividends) from here if you are an old-fashioned troglodyte who buys stock with cash. But for an eazy peazy fortune, just call your Goldman broker and order some December 2021 calls. For instance, 3900 strike calls expiring on that date can be had for $115 per share, meaning that you stand to make 3.5X your money just by closing your eyes, hitting the buy key and waiting for Goldman to send you the check for the $400 gain when its forecast comes true.

Then again, it needs be recalled that in their wisdom, sell side analysts now see December 2020 LTM earnings on the S&P 500 coming in at $91.80 per share, and then leaping upwards by 47% to $135.13 per share by December 2021. Yet even if the latter hockey stick should come true, the implied PE multiple at Goldman’s swell new December 2021 price target is 31.8X!

That’s right. If you shell out the $115 per share options premium you’ve got to believe that neither Sleepy Joe, nor Kamala Harris and her progressive-left comrades, nor the Covid, nor a gridlocked Washington, nor a confused or faltering Fed, nor any other untoward development will stand in the way over the next 14 months of a booming

return to economic normalcy, a 47% gain in profits and a PE multiple more than double the historic average!

Or, in the alternative, even at a frisky December 2021 PE multiple of 18X on that year’s reported earnings, the latter would have to post at $240 per share on an LTM basis to hit the Goldman target. Now, that would be up by 73% from the pre-Covid all-time peak of $139 per share in December 2019 and 164% compared to the (optimistic) Wall Street consensus for December 2020.

But, hey, don’t snicker. That’s the mighty Goldman Sachs reinforcing the mainstream narrative.

Just the same, and to paraphrase Abe Lincoln’s famous story about the man who was tarred, feathered and run out of town on a rail: If it weren’t for the honor of doing business with Goldman, we’d just as soon keep the $115.

Of course, Goldman doesn’t base its stock price forecast on the kind of earnings that CEOs and CFOs must report honestly to the SEC on penalty of jail time: Namely, GAAP net income.

Instead, they want you to believe that multiples are “reasonable” via the use of ex-items earnings, which are always 10-30% higher than reported earnings because they eliminate purported one-time gains and losses and non-cash items charged to the P&L in the current period like goodwill write-downs or restructuring provisions.

But here’s the thing. Anything that hits the income statement was a cash item at some point in either the past (e.g. goodwill) or the future (e.g. restructuring provisions) and if it carries a negative sign it represents a dissipation of corporate resources and value.

Likewise, eliminating one-time gains and losses is not a valid earnings-neutral smoothing procedure because in every quarter as far as the eye can see going back into the fog of ancient history, one-time losses always exceed one-time gains, and usually vastly so.

Thus, during the September 2020 LTM period, GAAP earnings posted at $97.68 per share or 19% below the Goldman-favored ex-items figure of $120.48 per share, while the shortfall in the June 2020 LTM figure was 21%.

For the last 12 quarters combined, the average ex-items figure of $142 per share was 16% higher than the GAAP figure of $122 per share. So you can take the “reasonable” PE canard with a grain of salt, but even then the current Goldman stock price forecast embodies the mother of all hockey sticks.

That is, ex-items earnings for the S&P 500 are now forecast by the street consensus to weigh in at $117.36 per share for the December 2020 LTM period, which figure Goldman projects to rise to $175 per share by December 2021.

So you have to believe that ex-items earnings will soar by 50% in just one year’s time and still be willing to pay 24.5X for said miracle of escape from a Covid/Lockdown shattered economy that shows exactly no signs at the moment of getting up on its hind legs and leaping skyward.

We do believe, therefore, that “unhinged” does aptly characterize the current mainstream narrative, and that’s in part because we think the imminence and efficacy of the vaccine silver bullet is way overdone; and also because despite the Fed’s best verbal flim-flam we do not think the laws of sound money have been repealed and that the Fed can keep monetizing 100% of Uncle Sam’s $2-3 trillion deficits indefinitely.

Yet, if there is no vaccine silver bullet next year, you will have the Virus Patrol re energized and completely unshackled under the nation’s new man of “science” in the Oval Office. Just this afternoon, for instance, one of Sleepy Joe’s closest helpmates— Gauleiter Andrew Cuomo of New York—decreed that anyone entertaining more than 10 guests in their own private home will be subject to fine and arrest for allegedly spreading the Plague.

Likewise, if the Eccles Building does not keep buying up Uncle Sam’s tsunami of supply, the bond market is a cataclysm waiting to happen.

As to the silver bullet, just consider what Pfizer actually reported. Namely, that from a trial pool of 43,538 participants they now have results for 94 individuals who tested positive for Covid-19, of which 86 were in the placebo group and 8 among those getting the two-shot vaccinations.

That’s how they get their ballyhooed 90% effectiveness claim, but we say, whoa!

That conclusion is based on only 0.216% of the trial universe, yet the company’s press release—-which enabled the CEO to sell 60% of his stock at a huge profit on Monday— contained zero information on whether the 94 cases were representative of the study population with respect to age, medical condition etc. and whether the actual Covid cases among the 94 reported to have tested positive were sniffles, mild, moderate, severe or death-threatening.

The truth is, the company’s press release amounted to nothing more than an (apparently) legal stock touting ad. Mr. Albert Bourla is now $6 million richer, but the most substantive thing contained in the press release not previously known was, well, this bit of soap-selling:

Today is a great day for science and humanity. The first set of results from our Phase 3 COVID-19 vaccine trial provides the initial evidence of our vaccine’s ability to prevent COVID-19,” said Dr. Albert Bourla, Pfizer Chairman and CEO.

This gets us to the point that the irrepressible Jon Rappaport keeps raising. To wit, why would anyone think that a 0.216% share of the trial universe is meaningful or reliable?

Moreover, why would the FDA go along with this, or especially the entire study protocol, about which the company’s press release conveys the following:

The trial is continuing to enroll and is expected to continue through the final analysis when a total of 164 confirmed COVID-19 cases have accrued

Yes, forget about the 43,538 participants and all the efforts to ensure its representative nature because Pfizer is going to quit when exactly 0.377% (164 participants) of the sample have reported.

A half-way attentive lay person might well say, WTF!

But having said that, he might upon modest further investigation also grasp the entire scam involved in fast-tracking the vaccine and the so-called Operation Warp Speed championed by the White House—the latter having been heralded as some kind of Republican “can-do” demonstration to the Swamp Creatures as to how a “businessman” like the Donald gets things done.

Well, no, not even close. The reason for shutting down the trial after less than one-half of one percent of the participants have been heard from is that in this day and age you can’t test a vaccine candidate by deliberately infecting a patient with the virus, most especially the unlucky folks who get the salt water tablet placebo.

Instead, what you have to do is put your feet up on a stool and wait for participants to contract the disease and become infected in the “wild”. That is, in their homes and on the highways and bi-ways of normal life.

But alas, Tony Fauci and his malpracticing doctors, the wanna be Robespierre’s they have unleashed among Blue State mayors and and governors, and the constant Chyrons of death running across the cable TV screens, have most of the sheeples, including those enrolled in the Pfizer study, scarred to death. So they do not leave home without their mask-up and without social distancing on the sidewalks, hallways and grocery store checkout counters.

So, then, how in the hell are study participants supposed to catch the Covid in the wild? Under the rules of ethics in these matters, the ones getting the real shot cannot even be told to get frisky and drop their mask every now and then in order to help the corporate folks at Pfizer complete their study and harvest their tens of billions of vaccine sales.

Needless to say, that’s why only 0.216% of participants (94) managed to get the Plague, which is allegedly running rampant in America, during the first three months of the trial; and why at that rate it would take 11 years to get a return from even 10% of the participants.

So there is a reason why it normally takes 3-5 years to do a vaccine trial: It seems that even the FDA is unwilling to let drug companies deliberately kill placebo-taking patients in order to speed up the process.

And that gets us to an even more insidious aspect of the silver bullet myth. Namely, because it takes so ungodly long for mask-up trial participants to get infected in the “wild” when the latter is operating effectively under economic martial law, the study

protocol assumes that any old case will do—even if so mild as to be barely symptomatic and readily cured with bed rest and drinking lots of liquids.

As Jon Rappaport noted regarding the generic case with all of these Covid-vaccine trials:

You see, the vaccine maker starts out with 30,000 HEALTHY volunteers. So, if they waited for 150 of them to come down with severe pneumonia, a serious case of COVID, how long do you think that would take? Five years? Ten years? The vaccine maker can’t possibly wait that long.

These 150 COVID cases the vaccine maker is looking for would be mild. Just a cough. Or chills and fever. That scenario would only take a few months to develop. And face it, chills, cough, and fever aren’t unique to COVID. Anyone can come down with those symptoms.

THEREFORE, THE WHOLE CLINICAL TRIAL IS DESIGNED, UP FRONT, TO FIND 150 CASES OF MILD AND MEANINGLESS AND SELF-CURING “COVID.” About which, no one cares. No one should care.

But, as we see, Pfizer is trumpeting their clinical trial of the vaccine as a landmark in human history.

What Rappoport is saying is that by the very nature of the Covid, the only point of a vaccine is to protect the small minority who develop severe cases owing to age, comorbidites or otherwise weakened immune systems, and especially those who suffer a life-threatening course of the disease. But as of the present, the CDC estimates that

about 88 million American’s have been infected—the overwhelming bulk of whom didn’t even know it because they were asymptomatic or experienced a mild-course of the disease and were home cured.

In fact, only 500,000 of these 88 million have been hospitalized according to CDC data as of yesterday. And based on the CDC’s expansive way of counting, the number of WITH-Covid deaths now stands at 231,000, a majority portion of which occurred in hospitals.

So no matter how you slice it, more than 87 million of the 88 million infected persons so far were in no mortal danger, and wouldn’t have been helped much even if Pfizer’s or any other vaccine had been available from day one.

So the question recurs: Among the 94 cases reported on Monday to the tune of a $1.5 trillion stock market rally, how many cases required hospitalization or involved even a serious home-cured course of the illness?

The company’s press release didn’t say, and when they run the clock to the FDA approved protocol’s 164 positive cases mark, they won’t say either.

That’s because, again, based on the any-case-will-do study design, the trial results cannot prove that the vaccine is effective in individuals who would otherwise suffer a severe course of the disease. In fact, based on the current national metrics, among any random universe of 164 infected people, exactly 0.57 persons would be hospitalized and 0.26 persons would die.

Alas, perhaps even the purportedly brilliant Mr. Kostin would agree that you can’t prove efficacy by comparing fractions of a person.

Nevertheless, out there in the “wild” after the vaccine is broadly distributed by, say, next June, the universe of the vaccinated will not be 8 souls who have contracted the disease under the Pfizer study to date, but tens of millions. And if it doesn’t work on the severe cases and even a few hundred deaths and/or hospitalizations are reported among the vaccinated, there will be panic in the already frightened streets.

As we said, the mainstream narrative is risibly corrupt.

Come to think of it, Goldman can keep its stinkin’ $115 lottery tickets, too.

The problem with Stockman's analysis is that it is rooted in the numbers everyone loves to lie about. Whether its profit margins, P/E ratios or debt ratios in the private and government world or Covid-19 and its case numbers and case/death ratio in the health world few of these numbers have enough accuracy to be useful. There are no easy answers to this but To the degree these numbers come from voluntary transactions is the degree to which they are trustworthy. Of course there is no way to predict with certainty when a transaction or action may turn involuntary. But since we know that voluntary transactions tend to be more trustworthy we need to move toward the voluntary and away from the involuntary. Identify and criticize involuntary action as always harmful and covid-19 will be reduced to the common cold it is and government spending to the theft it is. The way Stockman uses numbers borders on fear mongering.

ReplyDelete