Keynesian economists are annoying enough when they are pitching inflated financial assets on Wall Street or the supposed curative powers of fiscal deficits on Capitol Hill. But they become positively dangerous when they

populate the Eccles Building and usurp control of the nation’s capital and money markets lock, stock and barrel in the name of “monetary accommodation”.

Needless to say, the Fed is presently over-run with Keynesian money printers led by Janet Yellen and Stanley Fischer. Both of these famous PhDs are actually proponents of a primitive macroeconomic doctrine that should be called “bathtub economics”. In their wisdom, these doctors of economics have simply postulated that the nation’s economic output “should” be at aggregate levels which far exceed current production, and that the resulting shortfall from “potential” output, incomes and jobs is due to insufficient “aggregate demand”.

This purported “output gap” is conveniently self-serving. It has been interpreted to mean that the Fed has a plenary mission to fill-up the nation’s economic bathtub by generating sufficient incremental aggregate demand to off-set the shortfall. This demand plugging function, in turn, is to be accomplished by the constant intervention of the Fed’s open market desk into money and capital markets. So doing, it is empowered to manipulate, massage, twist, bend and pump any financial variable that in its wisdom is deemed to influence the transmission of its monetary policy (i.e.”aggregate demand” stimulus) into the real economy.

Except this is all a fiction. There is no such economic ether called “aggregate demand”; it is an utterly artificial construct of Keynesian economic models. What actually exists out in the real main street economy is nothing more than the total spending by households and businesses; and the latter does not pre-exist as an independent variable. Instead, it is derived from either current income or from incremental borrowing—that is, extending the pre-existing leverage ratio of business and household balance sheets to steadily higher levels.

But here’s the thing. The Fed can do only do two concrete things to influence these income and credit sources of spending—–both of which are unsustainable, dangerous and an assault on free market capitalism’s capacity to generate growth and wealth. It can induce households to consume a higher fraction of current income by radically suppressing interest rates on liquid savings. And it can inject reserves into the financial system to induce higher levels of credit creation.

But the passage of time soon catches up with both of these parlor tricks. When household savings decline to the vanishing point, as has occurred since the turn of the century, there is no more incremental spending to be extracted from current income.

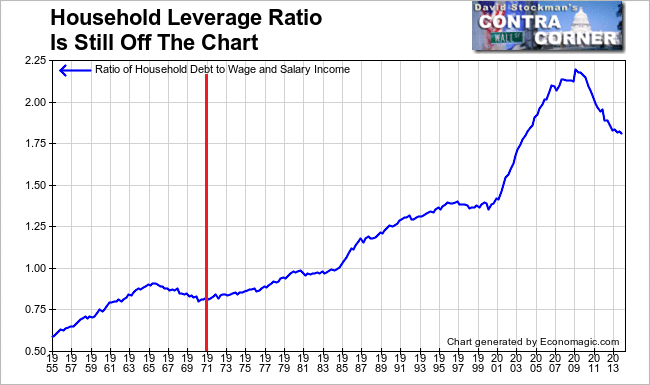

Likewise, when balance sheets become totally exhausted with leverage—as is also the case at present—there are no more one-time increments to spending available from the simple expedient of ratcheting-up household and business leverage ratios. That condition amounts to “peak debt” and it characterizes upwards of 90% of US households today.

Household Leverage Ratio – Click to enlarge

The fact is, the Fed’s modern regime of inducing lower savings and higher leverage was not only an unsustainable, one-time proposition that prevailed roughly from 1971 to 2007, but also was only good on the margins of Keynesian GDP accounting. It was the booster shot which stimulated a simulacrum of prosperity and out performance on the measured macro variables.

Still, none of the Greenspan/Bernanke/Yellen era financial market interventions and manipulations by the Fed could impact the foundation of spending—-that is, current period organic income. The latter comes from production, invested capital, entrepreneurial activities and labor hours and productivity.

Stated differently, income is the fruit of the economy’s supply side operations. But the central banking branch of the state has no tools to grow the supply side. The latter is the unplanned result of workers, entrepreneurs, savers, investors and inventors interacting on the main street market.

Take the case of labor hours. The crucial variable here is not some academic concoction called “full employment” or an arbitrarily chosen unemployment rate of say 5.2% measured against an artificially designated proxy for the work force collected by the BLS.

Instead, what matters is the price of labor; the quantity supplied everywhere and always follows the price. Accordingly, if at current production and income levels, the price of labor on the margin is too high, there will be elevated levels of unemployment. But the Fed can do nothing about millions of wage arrangements in the main street economy—-except to make over-pricing of labor worse by inducing households to live beyond their means on cheap credit.

To be sure, the Keynesian money printers claim they are boosting labor inputs by enlarging demand for the services of unemployed workers. But this just another case of the economist who tumbled into a 30-foot hole, but quickly assured his colleague of an escape plan: Assume we have a ladder, he airily intoned.

In a similar manner, the Keynesian economists who run the Fed have no ability to create the fictional ether called “aggregate demand”, yet they have seized control of the entire capital and money market pretending to do just that. However, not withstanding the fact that the Fed has pumped $4 trillion of new reserves into the financial system since the year 2000, there has not been a single hour of gain in private non-farm labor inputs supplied to the US economy during the past 14 years. Self-evidently, all their “assumptions” to the contrary, the Keynesian economists at the Fed do not have a magic ladder called “aggregate demand” that can pull idle labor hours into production.

Yet here is where the Wall Street connection enters the picture. While the modern Fed’s incessant manipulation of money market rates, the yield curve and the price of risk assets generally can have no lasting effect on household and business spending, it does cause massive financial bubbles. The latter, in turn, can be harvested by adroit speculators during the 5-7 year intervals between the inevitable busts which result from central bank financial repression and artificial inflation of risk asset values.

That essentially is the reason for the present universe of some $3 trillion of hedge funds, and the trillions more of mutual funds and institutional investors which surf on their momentum driving waves. Their assigned function in the scheme is to be the first-in and first-out as these central bank financial bubbles inflate and bust.

Naturally, it was only a matter of time before Wall Street sought to institutionalize these beneficent policies by developing a financial market overlay on the bathtub economics of the academic Keynesians. This new element originated during the Greenspan era with the expansion of staff to include Wall Street economists and traders. But the arrival seven years ago of William Dudley straight from the top economics job at Goldman Sachs took the matter to a whole new level.

In effect, under Dudley’s supervision the New York Fed has been transformed from a dabbler in the money markets to the plenary master of the entire financial system. Thus, during the early Greenspan days the nearly exclusive tool of Fed policy intervention was the Federal funds rate, but that was a crude and imprecise lever for managing the flow of incremental demand into the nation’s economic bathtub.

Accordingly, the doctrine of “monetary accommodation” was evolved by the Wall Street contingent at the Fed led by Dudley. By the lights of this new dispensation, any financial variable that might conceivably encourage more mortgage borrowing or corporate stock buybacks or “wealth effects” driven household consumption (albeit by mainly the top 10%) was fair game. Such variables were declared to influence “the transmission of monetary policy to the real economy”.

Thus, when Ben Bernanke averred a few years ago that the Fed’s success in stimulating the economy was evident in the soaring levels of the Russell 2000, he was merely noting a particular instance of this new monetary accommodation doctrine at work.

Yet the monetary accommodation doctrine surely does amount to an economic coup d’état by the unelected bureaucrats and academics who run the nation’s central bank. To be sure, they rationalize it in the name of their statutory mandate to achieve maximum employment and price stability, as contained in the Humphrey-Hawkins Act.

But read the act and the legislative history. Not even Hubert Humprhey himself ever envisioned a Fed which would target the Russell 2000 or deliberately punish main stream savers in order to inflate financial assets and encourage wealth effects driven levitation of the GDP and jobs count. The Fed’s plenary manipulation of prices across the warp and woof of the financial system thus amounts to the greatest instance of “mission creep” ever undertaken by an agency of the state.

Now in a recent forked-tongue effort to deny the existence of a Fed “put” under the stock market, Goldman’s plenipotentiary at the Fed, perhaps better referred to as B-Dud, has told us exactly that. If the monetary politburo deems that the nation’s economic bathtub is not full to the brim and therefore requires “extremely accommodative” policy, the central bank will indeed deliberately pump-up the S&P 500 to achieve its misguided ends.

A few weeks ago, the Fed’s hapless school marm and chair person lamented publicly about the severe shift of income and wealth to the top 1% during recent decades. Perhaps it is time for B-Dud to explain to her that its all about filling James Tobin’s economic bathtub with the requisite “aggregate demand”.

It goes without saying that Keynesian economists have always been a threat to free market capitalism. But now that they have hooked up with Wall Street agents like B-Dud they have become a clear and present danger.

….. we focus on how financial market conditions influence the transmission of monetary policy to the real economy. At times, a large decline in equity prices will not be problematic for achieving our goals….. (if) it does not conflict with our objectives. In contrast, when we want financial market conditions to be extremely accommodative—as has been the case in recent years when we have been far away from our employment and inflation objectives—then we will take into consideration a broad set of developments with respect to interest rates, the stock market and other measures of financial conditions in choosing the appropriate stance for monetary policy.

David Stockman was the Director of the Office of Management and Budget during part of the Reagan Administration, from 1981 to 1985. He is the author of The Great Deformation: The Corruption of Capitaism in America and The Triumph of Politics: Why the Reagan Revolution Failed.

Eurosystem Increasing Allocated Official Gold Reserves

ReplyDeleteThe Eurosystem is expressing an increasing interest in gold.

The fact the Eurosystem discloses the ratio between its allocated and unallocated gold and, more important, the fact that the portion of allocated gold is far greater and increasing, tells me the Eurosystem is allocating as much gold as they can. Add to that the Germans are currently repatriating over 600 tonnes of their allocated gold from the US and France, and The Netherlands has just repatriated 123 tonnes of its allocated gold from the US. Will the rest of the Eurosystem follow to repatriate their gold from abroad?

The Eurosystem is surely up to something with its gold. This can only be seen in advance of a reform of the international monetary system. As Jean-Claude Trichet, former president of the European Central Bank, stated on a financial forum in Beijing at the end of October 2014:

The global economy and global finance is at the turning point in a way… New rules have been discussed not only inside the advanced economies, but with all emerging economies, including the most important emerging economies, namely, China.

https://www.bullionstar.com/blog/koos-jansen/eurosystem-is-increasing-its-allocated-official-gold-reserves/

This is brilliant:

ReplyDeleteExcept this is all a fiction. There is no such economic ether called “aggregate demand”; it is an utterly artificial construct of Keynesian economic models. What actually exists out in the real main street economy is nothing more than the total spending by households and businesses; and the latter does not pre-exist as an independent variable. Instead, it is derived from either current income or from incremental borrowing—that is, extending the pre-existing leverage ratio of business and household balance sheets to steadily higher levels.

Further, I submit that the concept of "aggregate demand" effectively destroys in practice the concepts of both private property and any limitation upon government action. Instead of "demand" being the actual resources legitimately owned and controlled by free persons and available for voluntary exchange, "aggregate demand" implies that "demand" is a social[ist] phenomenon which can and must be manipulated by the government. One's actual resources are indistinguishable from wealth and purchasing power transfers resulting from Keynesian policy. All limitations upon the government's power are not gone as it becomes perfectly normal, necessary and constitutional for the government to loot and shift purchasing power based upon bureaucratic whim without any recognition of private property or due process of law.

It is nothing but a back-door commie plan.