Listening to Janet Yellen splitting hairs and blathering in circles about the state of the economy yesterday was enough to put you in mind of a paint-by-the-numbers robot built in the labs at MIT and programed by its Keynesian economics department. After all, the latter has also inflicted on the world Paul Samuelson, Stanley Fischer, and his infamous student, Ben Bernanke.

So why not a four-fer?

There is only one question that Yellen needs to answer and then all else is readily explained. To wit, does she actually believe that the money market rate——as formerly measured by Fed funds before Bernanke nationalized the interbank market in September 2008——is a wholly owned property of the FOMC?

Or does the overnight rate possibly have some measure of significance as a “price” in the financial system? And one that, in fact, is linked to the rest of the so-called yield curve, and from there to converts, equities, options/derivatives and the whole of the price discovery process in the money and capital markets.

Less than a decade ago almost every financially literate person knew the Fed funds rate—-even if increasingly massaged by the FOMC—- was a financial price and that it transmitted market signals throughout the financial system. So consider the implications of the Fed’s decision to keep it pinned to the zero bound for what will soon be 96 months running.

In a word, Yellen and her posse of Keynesian monetary central planners are apparently willing to drastically falsify the price of money and all that derives from it—-such as the bond market carry trades and the massive churning in the options pits—-on a virtually permanent basis.

And for what purported macroeconomic gains?

In a word, to achieve hairline increases in the inflation rate, when there is already too much inflation; and to nudge unspecified reductions in the US labor market’s “slack”, when the latter is almost surely beyond the reach of monetary policy in any event.

Stated differently, Yellen proved again yesterday—-and painfully so if you were watching her presser—that she is so robotically focussed on achieving fractional decimal point gains on the Fed’s so-called Humphrey-Hawkins “mandates” that she can’t see the forest for the trees.

The fact is,

ZIRP is planting multi-trillion dollar FEDs (financial explosive devices) throughout the entire financial system. Yet the FOMC majority still claims that there are no bubbles in sight.

Thus, the Yellen Fed is embracing giant financial risks for pure macroeconomic trivia. For instance, even if you assume that 2.00% inflation is some kind of magic economic elixir, how in the world can the denizens of the Eccles Building not admit that they are already there or certainly damn close?

The regular CPI adjusted for market rents—rather than the BLS’ specious measure of OER (owners’ equivalent rents)——was up 4.5% in the most recent year, and 2.4% since 2010. Likewise, the PPI for finished consumer goods is well above the Fed’s 2.00% target on a one-year and five-year basis, as is the core CPI.

Even the core PCE—the Fed’s absolute favorite measuring stick—– was up by1.6% on a Y/Y basis at the last reading. Isn’t that close enough for government work?

Indeed, the only price gauge that is materially “undershooting” the Fed’s inflation target is the headline CPI and there is absolutely no mystery as to why. To wit, the August CPI report showed that energy commodity prices were down 17.3% from prior year, while the CPI less food and energy was up by 2.3%.

In fact, if the Fed is eager for the tonic of inflation, there is plenty of it around. For example, services less energy were up 3.2%, medical care was higher by 5.1%, asking rents were up 5.6%, prescription drugs by 6.3% and health insurance by more than 9%.

So when Yellen was rattling on about under-shooting “our inflation goal” she wasn’t even grasping at straws; she was just emitting what has become a Keynesian ritual incantation that has no grounding in any kind of monetary history or logic. It’s just the cover story for the massive financial power grab undertaken by the Fed and other central banks since the turn of the century.

Yes, Yellen and her monetary politburo claim that Humphrey-Hawkins makes them go for every last decimal point of inflation—but that’s a self-serving crock. The Act was passed in 1978 before any economist—Keynesian or otherwise—had dreamed up the idea of inflation targeting by the central banks.

Actually, the statute’s “price stability” language called for a steady reduction in the raging inflation of the time—- until it reached 3.0% in 1983 and ultimately 0.0% by 1988. This long-run goal was purely aspirational, of course, and was the pound of flesh offered to conservatives by labor-Democrats who cared only about the “full employment” mandate”.

Nevertheless, it was enacted not by inflation lovers like Yellen and her posse, but on the heels of a ruinous double digit inflation that had scared the daylights out of main street America and the politicians who represented it.

On that score, I do have some authority because I was one of the latter. And while I was vehemently against the act and voted “no”, I most surely did not hear the bills sponsors—- Congressman Augustus Hawkins or the great liberal Democrat and thorough-going Keynesian, Congressman Richard Bolling——mention a word about the danger of inflation being too low. Nor did they even remotely suggest that the Fed would be obligated to pump unlimited credit into the financial system in order to achieve today’s sacred 2.00% inflation target.

That’s because this economically insidious target was not even invented until more than a decade latter. Moreover, it was the work of a tiny sect of fringe economist led by Ben Bernanke who had no democratic sanction whatsoever for inflation targeting, let alone 2.00%.

In fact, the very idea of an inflation deficiency wasn’t even conceivable until a few years ago. Yet a fundamental precept of our constitutional democracy is legislative intent; and with respect to the target of 2.00% minimum inflation, as measured by the shortest ruler available, there was no Congressional intent whatsoever in 1978—or for that matter in 1988, 1998, or 2008.

If the inflation mandate of Humphrey-Hawkins had any content at all, therefore, it was the fond hope that inflation would be ground steadily lower and that in the by-and-by it might even disappear entirely.

In the late 1970s no one saw any good in “moar inflation”. The only argument was about how rapidly it could be brought down, and whether or not there was a Phillips Curve trade-off between growth and inflation. Reaganomics, in fact, was a defiant rejection of that entire idea.

At length, however, even the GOP establishment forgot that rejection of the Phillips Curve in favor of supply-side economics had been the heart of Reaganomics. Otherwise, the GOP beltway mafia led by Karl Rove in the Bush White House wouldn’t have given Ben Bernanke the time of day—let alone appointed him to the Fed in 2002, and then promoted him to head the Council of Economic Advisers in 2005, and finally to head the Fed in 2006.

For crying out loud, the man was a hard-core Keynesian. He had given speeches about dropping money from helicopters, had advised the Japanese government to bury the islands in fiscal debt and believed that without constant “stimulus” by the state and its central banking branch market capitalism had a death wish that would inexorably lead to underperformance and depressionary collapse.

Yet even then, and notwithstanding Bernanke’s relentless prodding, the Fed did not formerly adopt inflation targeting and the sacred 2.00% target until 2012. Yet 5-years later we have a Keynesian robot in the top chair espousing mechanical adherence to an inflation goal that is not supported by a shred of empirical evidence.

In fact, the US economy would grow at a far more healthy rate at 0.00%inflation rather than 2.00%, and would do even better under a regime offalling nominal prices and wages. That’s because in an open global trading system, the price of goods is set by the China Price and the price of off-shoreable services—-like call centers, data processing and back office support services of every type—is set by the India Price.

In that context, good jobs get off-shored while the domestic job market gets bifurcated. That is, pay rates in higher-end jobs in finance, government, the professions and business management tend to equal or exceed CPI inflation while the lower-end jobs in bars, restaurants, stadiums, amusement parks, cleaning services and household help which can’t be off-shored or robotized—as of yet—are depressed by a massive overhang of labor market “slack” that Yellen doesn’t even remotely comprehend.

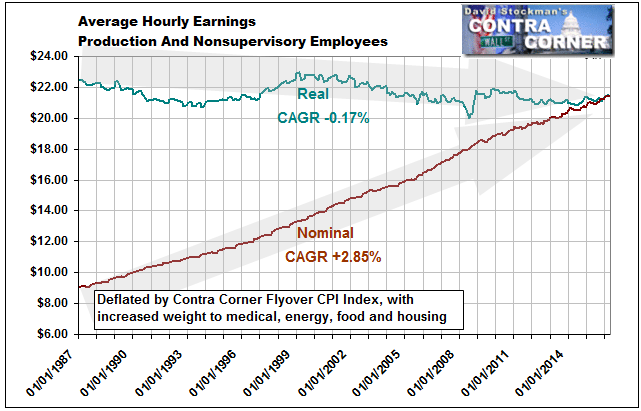

The chart below makes the point as well as anything else. The CPI has risen at a 2.1% compound rate for the last 29 years, even by the BLS understated measuring rod. Yet the very worst thing for main street jobs and incomes in America, was the near tripling of the average nominal wage rate shown in the chart. That caused jobs to be offshored in droves, while pay rates for the lower-end jobs left behind did not even keep up with the CPI.

The truth is, Yellen’s robotic commitment to the Fed’s spurious inflation goals is not merely laughable as an analytic matter; it is downright perverse and ruinous when it comes to the 90% of US households which do not own massively inflated financial assets or who do not have incomes which stay ahead of a domestic inflation rate that is anything but “deficient”.

When you properly measure the four horseman of inflation—food, energy, medical and housing—-over any sustained period of time and weight them for the budgets of the overwhelming share of households in Flyover America, you end up with huge increases in the cost-of-living that makes a mockery of Yellen’s blathering about a PCE deflator that is purportedly undershooting the target.

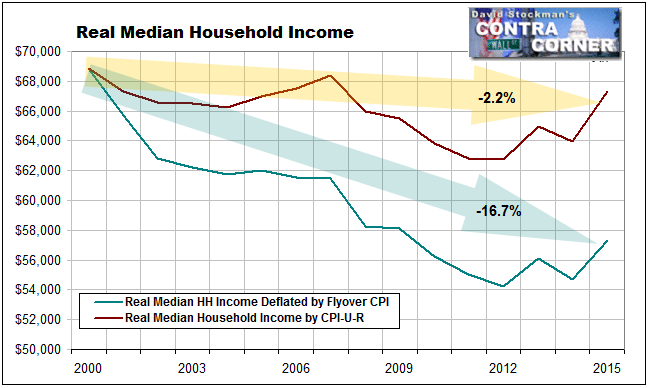

Not even close! The true cost of living represented by the Flyover CPI has risen nearly 40% more than the PCE deflator less food and energy during the last 16 years. That is, at 3.1% per annum, not the 1.7% rate about which Yellen so mechanically obsesses.

And that annual delta compounded over even a modest period of time makes all the difference in the world. Notwithstanding all of the recent ballyhoo about the phony 5.2% gain in real median household incomes for 2015, the median household income in Flyover America today is 17% below where it was in the year 2000.

Donald Trump recently suggested that Janet Yellen should be “ashamed of herself” for playing politics with the Fed’s printing presses.

He was too kind. She should be fired for gross incompetence and for inflating a hideous financial bubble that will bring untold ruin when it finally implodes.

David Stockman is the former Director of the Office of Management and Budget during part of the Reagan Administration, from 1981 to 1985. He is the author of The Great Deformation: The Corruption of Capitalism in America and The Triumph of Politics: Why the Reagan Revolution Failed and Trumped! A Nation on the Brink of Ruin... And How to Bring It Back

Hmmm... I wonder why Stockman is still using the term ZIRP to describe the current rate environment. Rates pinned to the "zero bound" for 96 months running as well. Doesn't he know the Fed bravely and in the face of its critics, including so-called Austrian-lites, "raised rates" last year?

ReplyDelete