By David Stockman

There is about to be a changing of the guard in the Eccles Building. That comes straight from the tweeter-in-chief, who actually verbalized his thoughts on the matter during interviews yesterday:

I tell you what, she was in my office three days ago. She was very impressive. I like her a lot. I mean, it’s somebody that I am thinking about......(but) I have to say you’d like to make your own mark....

We'll take the bolded phrase as gold watch time for Janet Yellen upon expiration of her term in February. And with a full measure of Trumpian gusto, we'd also say:

GOOD RIDDANCE!

When the story is finally written about how capitalism was strangled and America impoverished during the first quarter of the 21st century, Janet Yellen will rank high on the list of villains----right along with Ben Bernanke and Alan Greenspan.

Their unforgivable sin was to systematically falsify the most important prices in all of capitalism-----the prices of money, debt and other financial assets.

They did so in the arrogant and erroneous belief that 12 mortals on the FOMC can improve upon the work of millions of consumers, producers, workers, entrepreneurs, savers, investors and speculators on the free market; and that it's possible to centrally plan and manage a $19 trillion economy by fiddling with interest rates, manipulating the yield curve and massively and fraudulently monetizing the public debt.

For want of a better term, we refer to this entire, misbegotten Greenspan-Bernanke-Yellen doctrine as Bubble Finance. That's because in an open world economy flooded with cheap labor and capital, current Fed policy ultimately generates destructive financial bubbles on Wall Street, not sustainable prosperity on main street.

In fact, the evidence is now overwhelming that Bubble Finance unequivocally weakens domestic investment and growth and erodes real wages and living standards. In part that's because it induces corporate C-suites to strip mine cash flows and balance sheets in order to fund financial engineering schemes (stock buybacks and M&A deals), thereby pumping trillions of cash back into Wall Street; and in part because it blocks domestic cost-price-wage deflation, thereby accelerating the off-shoring of production, jobs and earned incomes to lower cost venues abroad.

At the same time, Bubble Finance fuels the massive inflation of financial asset prices because, under current conditions of Peak Debt, the Fed's flood of liquidity and credit never leaves the canyons of Wall Street; it simply funds trading leverage and the bidding up of the prices of existing securities. So doing, these central bank intrusions capriciously redistribute wealth to speculators and the top tier of households which own most of the financial assets.

The evidence for the damage to main street is clear as a bell if you disregard the Wall Street/Washington lie that a once-in-500-year financial disaster struck the US and world economy in September 2008, and that it was only "extraordinary" monetary measures and central bankers' "courage" to print that precluded Armageddon.

Not at all. There never was a real financial meltdown or run-on-the-banks outside of the canyons of Wall Street.

Had the free market been allowed to have its way with the speculators, gamblers and leverage artists, the AIG holding company would have been liquidated; state insurance commissioners would have taken over its subsidiaries to protect policy holders; the mortgage securitization meth labs of Wall Street would have been shutdown; the duration and credit mismatched trading books of dealers would have been crushed; and Goldman Sachs and Morgan Stanley would have been forced into Chapter 11 and reorganized into numerous smaller and more prudent financial services firms.

It would have all been over in a few months, and the crony capitalists and gamblers who had been enabled by the post-1987 era of Bubble Finance would have been carried out on their shields. So, too, the Greenspan Put would have been interred and honest price discovery would have been restored to the nation's financial markets, thereby giving capitalism a new lease on life.

As it happened, the post-Lehman shock to the C-suites of corporate America ended on its own accord after about nine months of severe liquidation of excess inventories, bloated payrolls, failed M&A deals and underperforming assets----all of which had been enabled and accumulated by 20-years of Bubble Finance.

As we have demonstrated elsewhere, however, the natural regenerative forces of capitalism were already at work by the summer of 2009. A self-fueling business recovery was underway long before Obama's shovel-unready fiscal stimulus got going or any of the Fed's zero cost money made its way to main street.

Indeed, the Fed's $3.5 trillion bond buying campaign and various phases of QE had no impact whatsoever on triggering, sustaining or enhancing the natural business recovery that is now nearing its 100th month.

To be sure, this recovery has been the weakest in history by a long shot. But that's not owing to the after-shock of a financial plague that arrived on a comet from outer-space, as the Fed and its acolytes risibly insist.

To the contrary, the Wall Street meltdown was caused by Bubble Finance, while a weakening GDP growth rate is the inherent consequence of excessive financialization, burgeoning debt and the diversion of business cash flows and capital into secondary market speculation. And by doubling down on Greenspan's giant errors, Bernanke and Yellen only compounded the harm.

That is, it caused main street growth to become even weaker and Wall Street bubbles to become even larger and more dangerous.

As to the former, you can't argue with the chart below. Real final sales strip out inventory fluctuations and thereby provide a reasonable approximation of the over-the-cycle trend in output growth.

Self-evidently, the final phase of Bubble Finance has nearly ground economic growth to a halt. And unlike the central bankers' statistical shenanigans which leave out the recession quarters, we measure on a peak-to-peak basis because modern recessions do not come from outer space or inner greed; they are caused by central bankers.

Moreover, we are quite confident that the 1.2% growth rate for 2007 to 2016 is not going to get any better with whatever time remains in this cycle----even as it pushes up against the historical record of 118 months.

In fact, the US economy is visibly slumping by virtually every measure of main street activity---from weakening auto production to faltering housing starts and punk productivity. But unlike all the available government massaged measures, the one that never lies-----wage and profits taxes forwarded to Uncle Sam by employers and companies----is flashing a bright red warning.

To wit, since August 1, Uncle Sam has collected $660 billion in income, payroll, corporate and excise taxes. But that number, large as it seems, is only 0.7% higher than the $656 billion collected during the same period last year.

Accordingly, factor in CPI inflation at around 2% and you have an economy that is dead on the water or actually sinking below the flat-line.

At the same time, the egregious reverse Robin Hood effects of Bubble Finance cannot be gainsaid. Indeed, the chart below constitutes a screaming bill of indictment against our now retiring Keynesian school marm and her cowardly fear of Wall Street.

This is what 100 months of ZIRP, free carry trades, massive yield suppression and the rank idiocy of "forward guidance" (i.e. telegraphing to Wall Street speculators every central bank move, including the exact cusip numbers of bonds to be purchased) has produced. Since the pre-crisis peak, the bottom 80% of US families have actually experienced a shrinkage of their net worth.

Virtually all of the gain has gone to the top 10%. And if you unpeel that onion you would find that the average $700,000 gain per family shown below is heavily weighted by the gargantuan gains of the 1% and even the 0.1% of billionaires among them.

Needless to say, nothing remotely like this outcome would happen on the free market. Honest capitalism, in fact, really does lift all boats.

So we really do mean good riddance to Janet Yellen. She has not only presided over policies that have punished main street workers, savers and businesses while showering the elites with unspeakable windfalls, but has also forced the rest of the world to follow the mad money printing policies of the Fed.

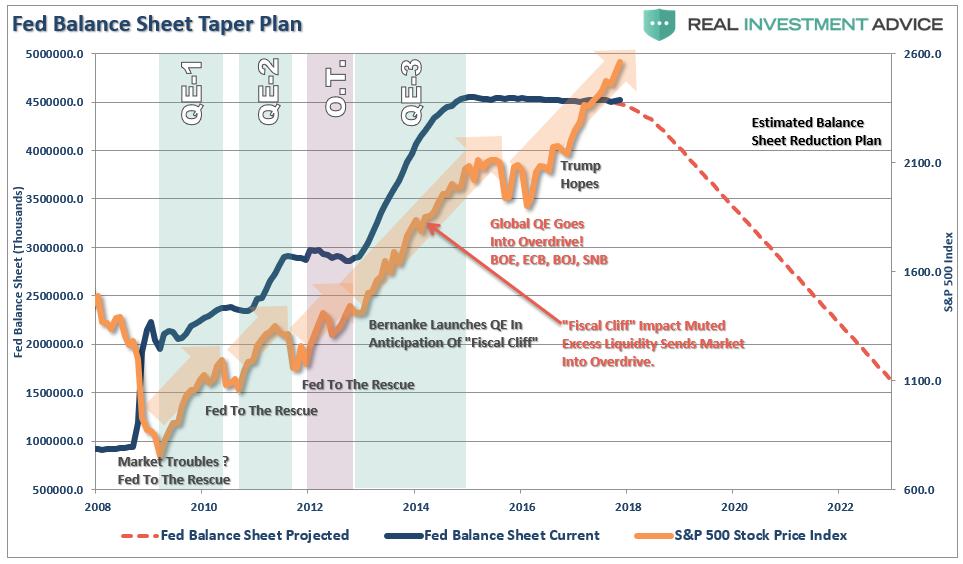

The great problem for her successor---whether it's a crony capitalist Keynesian like Jerome Powell or Milton Friedman's dangerous disciple, Professor Taylor------is that they will have no choice except to crawl off these 5X eruptions of central bank balance sheets (7X in the case of the Swiss central bank).

Needless to say, as the era of balance sheet shrinkage gets fully underway----and even the ECB acknowledged this morning that it will----QT (quantitative tightening) will cause yields to soar in the world's $100 trillion bond market and pricing and valuations for all other financial assets---especially junk bonds and equities----to be reset accordingly.

Here is one depiction of what the Fed's balance sheet might look like going forward during the coming era of QT and demonetization.

It's the reason why no one in their right mind should still be buying the dips.

It's also the reason why a fiscal crisis in the Imperial City is just around the corner---all the more so if they manage to pile $1.5 trillion in tax cuts on top of the $31 trillion in national debt that is already baked into the cake by 2027.

Upon Janet Yellen's leave, it is also the reason why the new watchword should well and truly be expressed in the Donald's own patented style: LOOK OUT BELOW!

The above originally appeared at David Stockman's Contra Corner and is reprinted with permission.

No comments:

Post a Comment