By David Stockman

You would think that knuckleheads like Senate GOP Leader Mitch McConnell would finally wake up. Last night the biggest spender since LBJ and FDR combined laid-out Part 3 of a $6 trillion in 100 days spending spree—which comes on top of the Donald’s $4 trillion fiscal bacchanalia last year. Yet the bond vigilantes barely wiggled their small toe.

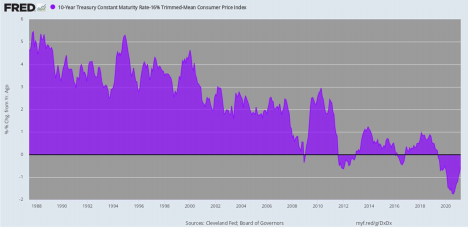

Indeed, at 1.65%, the 10-year UST is still buried deep below the running inflation rate, which rate itself is on the verge of lift-off.

Still, today’s negative 50 basis point real yield on the benchmark UST is only the culmination of a 30-year campaign by the Greenspan Fed and his heirs and assigns to destroy honest price discovery in the bond pits on the misbegotten theory that cheap debt fosters growth, prosperity and wealth.

No, what it actually does, among countless other ills, is unshackle the politicians to bury future generations in unspeakable debts.

Read the rest here.

Thus, if the real spread on the 10-year (purple area) was even +200 basis points, as it was at the turn of the century, the 10-year UST would now be yielding 4.25%. At that level, even Easy Janet (Yellen) would not have blessed Sleepy Joe’s $6 trillion spend-a thon and centrists like Senator Manchin would have been a lot more than merely “uneasy” upon its presentation to the Congress.

33-Year Destruction Of Honest Bond Prices By The Fed: 10-Year UST Yield Minus Inflation

So we actually do understand what the Biden Administration is doing. With what amounts to free money on offer, the Progressive/Left has spotted a once in a lifetime opportunity to saddle the American public with the kind of Cradle-to-Grave Stimmy that they have always dreamed about.

Until recent times, of course, they were invariably stopped cold by the bond vigilantes, which is to say, honest yields in the UST trading pits. But now the bond vigilantes have been lobotomized many times over and the denizens of the once-and-former party of the old time fiscal religion are waking up this morning to wonder what hit them.

After all, how do you compete with free maternity leave, free child care, free pre-school, free elementary and secondary education, free community college, nearly free university, virtually free ObamaCare, free elderly care and, to boot, after $3,600 per child tax credits, essentially no income taxes at all for upwards of 75% of adult Dem voters?

That is, the Dems are going with universal free stuff for all while the going is good. The rather despicable Svengali who ran the Obama White House and then ran Chicago into the ground from the mayor’s office, Rahm Emanuel, made that clear as a bell when he explained the Dems’ true political calculation this week to the Washington Post:

“Once everyone’s in, all the parents want in. Then it’s not a poor person’s program or a poverty program. It’s an education program. . . . That to me, that is essential. It changes the center of gravity once it’s for everybody.”

So now Sean Hannity and his Foxified Republicans are belatedly waking up, emitting a cloud of purple rhetoric about the impending fall of America to socialism.

But we have a news flash: Financial socialism has been underway for several decades now because on Wall Street all the boys and girls get a trophy, while risk and loss have been essentially vaporized by the central bankers.

So the Dems are making bold to extend those blessings to the unwashed masses and have drafted the central bank as their fiscal handmaid. After all, do you think that JayPo thinks he has a snowball’s chance in the hot place of being reappointed when his term ends next year if he doesn’t keep on monetizing $120 billion of Uncle Sam’s prodigious emissions each and every months, at least?

In its morning editorial, the Wall Street Journal got that part right:

We’d call the price tag breathtaking, but by now what’s another $2 trillion? Add $2 trillion or so each for the Covid and green energy (“infrastructure”) bills, and that’s $6 trillion of new spending in 100 days. That doesn’t include the regular

federal budget of more than $4 trillion a year. No worries, mate, the Federal Reserve will monetize the debt.

So the question recurs. Where was the GOP when the props were being pulled out from under fiscal rectitude by the Fed per the chart above?

Alas, to a man and woman—-except for Ron and Rand Paul and a handful of others— they have been AWOL for the better part of three decades on the single most important requisite of capitalist prosperity: Namely, sound money and honest free market price discovery in the money and capital markets.

Indeed, three of the four worst Fed Chairman in its history—-Greenspan, Bernanke and Powell—were appointed by Republican presidents, while the Republican members of the House and Senate financial services committees regularly tripped over each other genuflecting to these prosperity-wreckers during their periodic appearances on Capitol Hill.

It was not always this way. Your editor, the late Congressman Jack Kemp, Senator Paul Laxalt and some others actually got a gold standard plank in the 1980 GOP platform. And during the brutal inflation purge necessarily conducted by the great Paul Volcker thereafter, most Republicans stood their ground for sound money and relieved themselves of whatever dalliance with Keynesian economics they had been infected with during the Nixon era.

Unfortunately, the easy money Texas pol who got the US Treasury brief during the Gipper’s second term, Jim Baker, effected the most destructive financial decision of modern times.

Paul Volcker was by no means ready to leave his post when his second 4-year term expired in 1987, nor should he have. But Baker, who didn’t much believe in sound money, forced him to retire per an alleged understanding at the time of his 1983 reappointment.

By 1987, however, Volcker had proven himself to be the greatest Fed chairman in its history and more suited than any one else to complete the task of restoring a semblance of sound money after the inflationary disaster of the 1970’s.

Unfortunately, the uncured Reagan deficits were starting to catch-up. That is to say, the US economy was booming after Morning in America incepted in late 1983 and the bond vigilantes were soon having their way in the bond pits.

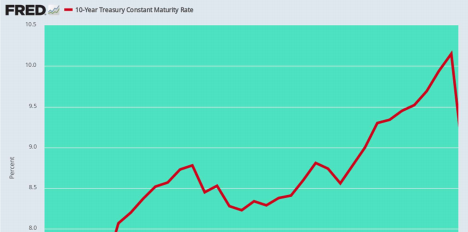

As it happened, the 10-year yield had fallen from 16% to a low of 7.1% in February 1987 in response to Volcker’s conquest of inflation. But owing to still $200 billion deficits as far as the eye could see, that’s all she wrote.

In a classic “crowding out” sequence, rising private demand for capital came crashing up against Uncle Sam’s ample elbows, causing rates to head swiftly skyward. During the next nine months the benchmark yield rose by more than 300 basis points—until the newly installed Greenspan essentially cried Uncle in the aftermath of Black Monday on October 19th and turned on the printing presses, full speed ahead.

Little did the world yet know, but then and there the death dirge of the bond vigilantes incepted and the GOP’s amnesia about sound money and fiscal rectitude began its long ascent.

You can blame this pivotal inflection point on Baker because the Gipper was a sound money, gold standard man at heart. Reagan would have likely reappointed Volcker on his own motion, but his diary from March 16, 1987 makes clear why that didn’t happen:

Then Jim Baker—re the Aug. end of the term for Volcker as Chrmn. for the Fed. Reserve Board. We are going to see if Alan Greenspan will take the job if Paul will step down gracefully.

The fact is, Baker didn’t want rising rates and a crowding-out driven recession in front of the 1988 election because his Texas friend and mentor, George Bush the Elder, was next in line. So he had convinced Reagan that Volcker had to go and that Alan Greenspan was just as sound on money matters and a Republican to boot.

In fact, back in the day (the 1950s and 1960s) Greenspan had been a gold standard believer and even a sometimes member of Ayn Rand’s coterie. But after going to Washington as Ford’s CEA chairman in 1974, his true colors materialized.

That is, he proved to be less a man of conviction than one of conviviality. He desperately wanted to be accepted by the powers that be in Washington, and at length to be lionized by them.

In any event, he stopped the bond vigilantes cold in the fall of 1987 and thereafter kept the bond pits flush with whatever fiat credit was needed to keep interest rates in check and a generational financial boom gathering stream.

Last Act of the Bond Vigilantes, Eruption of 10-Year Yield In 1987

To be sure, during the 1990s and thru the end of Greenspan’s term in January 2006 the rise of new technology and the internet did give a boost to economic performance. Still, there is no doubt that financialization was Greenspan’s signature legacy.

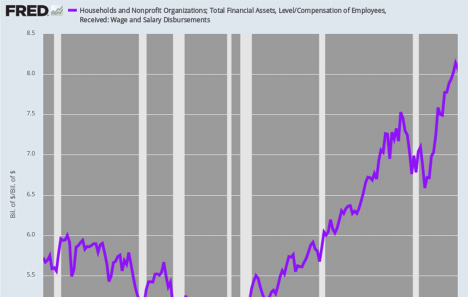

During his tenure, main street households experienced a 165% gain in wage and salary income, even as their financial assets soared by 280%. As a consequence, the 5.7X ratio of financial assets to earned income in 1987, which had prevailed in that zone during the decades of post-war prosperity, soared to 8.4X by the time Greenspan left the Fed in Q1 2006.

Ratio of Household Financial Assets To Wage And Salary Income, 1987- 2006

Here’s the thing. All that fantastic inflation of financial assets got intermediated by Wall Street one way or another. As a result, the center of lobbying power on the GOP side of Washington subtly but steadily shifted over time.

That is, when the big Reagan budget cut and tax cut packages were passed by a Democratic Congress in 1981, it was due to the fire power of the main street lobbies from back home.These included local bankers, home-builders, car dealers, real estate agents, life insurance agents, drug store operators, lumberyards, small manufacturers, wildcat oil drillers, main street merchants and doctors, lawyers etc.

They all hated big deficits, high interest rates, intrusive Washington bureaucracy and Big Government generally. And it was, in fact, the main street business lobby and relatively honest money that kept Leviathan in check.

As Greenspan took his bows 25 year later, however, the center of lobbying power had shifted to Wall Street and the financial industry, even as Greenspan’s decades of Keynesian central banking and easy money had sent the bond vigilantes into permanent hibernation.

Needless to say, the financial industry knows whereupon its bread is buttered, and has functioned as the Fed’s potent advocate and shield in the political wars of Washington.

At length, therefore, the GOP members of the House and Senate finance and banking committees were bought and paid for by the new financial industry lobbying power. Soon, nary an ill-word was spoken about the Fed from the Republican side of the aisle, even as it destroyed honest price discovery in the bond pits and gutted the bond vigilantes that had kept the old main street lobbies vigilant and the GOP wedded to its old time fiscal religion.

Alas, last night they found out to their shock and dismay that the rogue central bank they manned, fostered and coddled for three decades has now paved the way for a genuine social democratic, free-stuff-for-all moment in American political history.

Of course, what remains of the Trumpified GOP actually believes that the real problem in America is that the Donald’s idiotic wall on the Mexican border remains unfinished and scheduled for effective demolition.

Soon they will find out, however, that it is not Hispanic immigrants looking for work in America that voted them out of office. It was the 12 unelected money-pumpers on the all-powerful FOMC—an American monetary politburo—that allowed their political enemies to finance social democracy by monetizing the mountains of debt that have been and will be issued to finance it.

This AM some right-wing pundits posted the above warning about the import of Sleepy Joe’s spend-a-thon. Except, other than some symbolic tax nicking of the 1% that may yet happen, the slogan would better read, “monetizing our way to prosperity”.

That’s really how we got here.

The above originally appeared at David Stockman's Contra Corner.

No comments:

Post a Comment