By David Stockman

You really cannot curse Donald Trump enough for his horrid appointments to the Fed. The latter is now and has been for a good while the implacable enemy of sound money, fiscal rectitude, capitalist prosperity, small government and personal liberty.

In fact, the Donald’s last appointment, who was confirmed in the nick of time in December 2020, just averred that 4.0% inflation would be just fine by him:

Among Fed speakers overnight, Governor Christopher Waller signaled that rates won’t rise until policymakers either see inflation above target for a long time or excessively high inflation. He also said he would only get worried if inflation rose above 4%, defining the Fed’s first real “red-line.”

Well, what would you expect from this paint-by-the-numbers academic?

After graduating from Bemidji State University (whatever that is) and getting a PhD in economics from Washington State, he spent his entire career professoring, writing papers in behalf of easier money and more Fed power, and eventually heading the “research” department at the St. Louis Fed, where he teamed up with its lunatic dovish president, James Bullard.

Read the rest here.

In other words, just the kind of guy a Republican president should put on the nation’s monetary politburo!

Well, actually it’s worse. It seems that the Donald had first reached out to Waller’s boss, the aforementioned James Bullard, who said “no” only because he didn’t want to move to Washington DC. But as a favor to the Republic, the St. Louis Fed president recommended his deputy and, as it turns out, the professor who had taught Bullard his screwball monetarist economics in the first place.

Needless to say, the Donald’s embrace of these two monetary socialists alone puts paid to the conservative delusion that Trump was the great white hope in the endless battle against leftist aggrandizement of the state.

And, yes, we do use the term “socialist” advisedly because at the heart of this misbegotten creed is the notion that the state, not private actors on the free market, must make the big decisions about economic and social life. Yet in this day and age what could be bigger or more consequential than the price and allocation of money, debt and other financial assets?

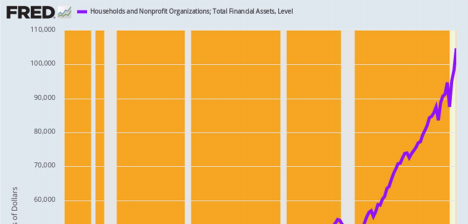

During the last 43 years, in fact, total financial assets held by the household sector have increased by a staggering $100 trillion. And that’s just a proxy for the massive levels of bank deposits, money market funds, bonds, publicly traded shares and private equities which flow through the warp and woof of the nation’s $21 trillion GDP.

In a word, socialist central planning has been elevated to a new art form based on control of the economy from the commanding heights of finance. That’s what today’s version of Keynesian central banking is all about and it’s damn evident, but totally ignored, in every Fed meeting statement, presser and policy speech.

To wit, central banks were once in the money business, in the sense of securing its availability, liquidity and stable value. But the contemporary Fed never says a peep about the place where money arises and dwells—the financial markets—while gumming endlessly about the main street economy and the condition of and its targets for the components and constituents of GDP.

That’s socialism by any other name, but through a Gosbank of finance, rather than a Gosplan of industry. Yet, ironically, it’s leading to the same outcome as in the old Soviet Union: Namely, a failing economy for the masses and a concentration of wealth and privilege among the tiny elites who are close to the levers of control.

Total Household Financial Assets, 1977-2020

Indeed, the very vocabulary of our monetary politburo tells you all you need to know. For instance, shortly after Waller’s nomination to the Fed, he told Bloomberg in no uncertain terms that setting the price of money was the prerogative of the state, not investors on the free market who have real skin in the game:

We didn’t see any overheating in the economy coming, so the question was: why are we raising rates?’’ Waller said in an interview June 25 with Bloomberg Radio’s Kathleen Hays. “We didn’t see any reason to raise rates just for the sake of raising rates.’’

No, that’s the wrong question!

The right question is why has the Fed spent 13 years capping and smothering the money market rate in the first place. And that they have done in spades.

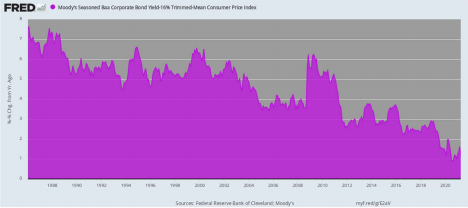

The chart below shows the real Fed funds rate, calculated by subtracting the YoY trimmed mean CPI increase from the Fed’s target rate. During the last 169 months (since March 2008) the rate has been deeply negative most of the time and just a tad positive for a grand total of 7 months, all in 2019. And now, after last year’s money printing orgy—the real Fed funds rate stands at -2.37%, nearly the deepest level ever.

Of course, never in a million years would participants in voluntary exchange on the free market lend money—even overnight—at a negative real rate 96% of the time over a 13 year period. It defies economic logic and sanity itself.

No, this is the work of the American Gosbank, laboring under the delusion that interest rates are the magic control dial by which the multitudinous ebbs and flows of the mighty $21 trillion US economy can be brought to heel and marched to target.

The very idea is hideous, but what is more hideous is that James Bullard and Christopher Waller have been key theoreticians of the interest rate theory of Gosbanking. Call them the Marx and Engels of central bank-based socialism and be done with it.

Yes, and it was these cats—unelected, unaccountable, dangerous and dead wrong—that Donald Trump wanted to put in charge of American capitalism.

As we have been wont to say, Orange Man gone, and thank heavens! Real Federal Funds Rate, 2008-2021

Needless to say, these new mechanisms of socialist control, just like in the old Soviet Union, were not remotely up to the task. Among the manifold failings and ills in the latter was the fact that central planning tended to produce enormous unintended and malign effects owing to erroneous incentives and price signals.

For instance, Soviet nail factory managers like all others got measured and rewarded by the tonnage produced. So the story goes that one enterprising chap massively exceeded his quota by producing only ten-ton nails!

Effectively, that’s what is happening in the financial markets today. The Gosbankers are aiming at the PCE deflator and the U-3 unemployment rate, but the enormous injections of liquidity designed to keep the interest rate control dial on target never really leave the canyons of Wall Street.

Instead, they radically inflate the price of financial assets and deflate the carry cost of debt, thereby causing economic actors to ape the Soviet nail factory manager. For instance, the C-suites foolishly cripple their balance sheets by allocating trillions to financial engineering maneuvers such as stock buybacks and uneconomic M&A deals.

The reason is simple. Debt has been made so dirt cheap in real terms (after inflation) that top executives can pull down tens of millions of stock option winnings by the expedient of borrowing money or allocating cash flow (which is the same thing) to shrinking their share counts via buybacks and M&A deals; or, in the alternative, they can pay rich dividends, knowing that when a rainy day might come they can borrow funds cheaply on Wall Street.

And we do mean cheaply. Back in 1987 when Greenspan was launching today’s version of monetary central planning, the most common corporate bond—investment grade BBB issues—carried a real interest rate of 7%. Since then its been a relentless march downhill, with today’s real yield posting at just 1.5%.

Again, this isn’t just a fun fact from the St. Louis Fed’s data base; it’s an everlasting affront to the free market because no way, no how, would voluntary exchanges of 7-10 year money occur at a 1.5% real yield. Not when we are talking BBB corporate bonds, where the risk of loss is palpable, standing as they do one notch away from junk grade.

Real Cost of Corporate BBB Bonds, 1986-2021

Indeed, in junk bond land itself the distorted price signals would actually make the Soviet gosplanners proud. That’s because junk bonds are almost never used to fund productive investments in plant, equipment, technology and labor skill enhancement.

To the contrary, the overwhelming use is to fund LBOs, special dividends to private equity owners, over-priced M&A deals and share buybacks by less than investment grade companies.

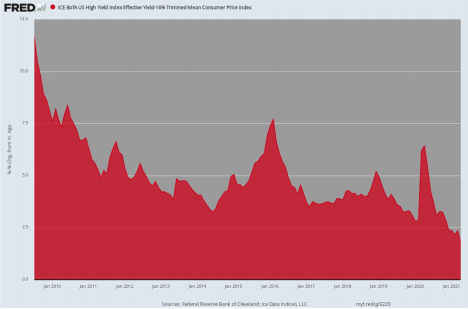

The chart below shows how close we are getting to the ten-ton nail. As of April 2021, the real cost of high-yield debt is just 1.79%, the lowest level since the original issue junk bond was pioneered by Michael Milken back in the early 1980s.

So when fools like Christopher Waller say they are keeping interest rates buried in the sub-basement of history because there is no inflation for the Fed to worry about, and won’t be until inflation rates shoot above 4%, here’s what they are accomplishing.

To wit, they are causing a false flow of investable funds into the junk bond market as fund managers desperately search for yield, even to the point of having their Wall Street bankers make the rounds of C-suites peddling junk funded financial engineering schemes; or, worse still, banging on the doors at private equity shops urging them to do leveraged recaps so that fund managers can gather assets and private equity owners can buy another yacht.

Real Junk Bond Yield, 2009-2021

At the end of the day, the sweep of these continuously wrong price signals and incentives amounts to this: It causes the economic equity base of American business to be liquidated through stock buybacks and cash funded M&A takeovers, thereby goosing prices in the shrunken pool of equities which remain outstanding.

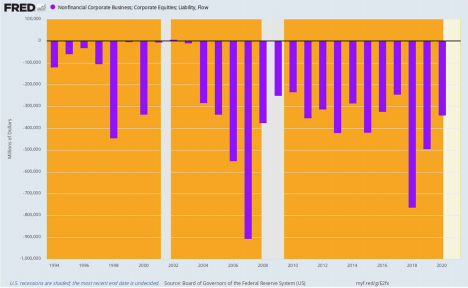

For want of doubt, here is the net equity flow into the US business economy since 1994, as tracked by the Federal Reserve itself. During that 26-year period, there was but a single year (2002) when nonfinancial corporations raised a positive amount of net equity, while liquidating a total of $8 trillion of book equity over the period.

Stated differently for the better part of the last three decades—spurred on by the money printers in the Eccles Building—the C-suites of corporate American have liquidated an average of $310 billion of corporate equity year-in-and-year-out. Effectively, they are running glorified hedge funds, not main street businesses.

Net Corporate Equity Raised or Liquidated, 1094-2020

There is no mystery, of course, as to where all the corporate cash used to buy back shares and buy out other companies went. It was just another case of the Willie Sutton principle—the legendary criminal who said he robbed banks because that’s where the money was.

Likewise, when the C-suites rob their balance sheets to goose their share prices and options value, the overwhelming share of the benefit goes to where the shares are owned. That is to say, to the top 1% and 10%, who own 40% and 71% of the stock, respectively, and the top 20%, who own 93% of the total.

In other words, Fed heads like Waller yammer endlessly about their macro goals for the main street economy, but the bottom 80% of households don’t get a damn thing from the Feds massive inflation of financial assets generally and the stock market particularly.

In that respect, when it comes to the task that the free market, not the central banking branch of the state, is suited for—generating rising living standards and real, sustainable wealth—the Fed, like the Soviet gosplanners, is producing a lot of useless 10-ton nails.

Actually, it’s worse. Besides useless and unfair financial windfalls to the top of the economic ladder, the Fed’s massive interest rate repression has destroyed fiscal rectitude entirely, thereby unleashing the Leviathan on the Potomac like never before.

We were reminded of that today by the fiscal year-to-day budget numbers. After 7 months, the Federal deficit has clocked in at $1.9 trillion, 28% higher than last year’s out-of-this world $1.48 trillion.

More specifically, outlays totaled $4.07 trillion during the period, while revenues posted at just $2.14 trillion. That is to say, the Banana Republic-worthy politicians on the Potomac borrowed fully 48% of what they spent.

Come to think of it, thanks to the Fed—with the help of the clowns like Waller that the Donald appointed to its Board—-America’s politicians are behaving more and more like the Soviet nail factory manager, generating massive debts and intrusions which will eventually sink the economy as surely as did Soviet communism in an earlier era.

David Stockman was Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street.

David Stockman was Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street.The above originally appeared at David Stockman's Contra Corner.

No comments:

Post a Comment